As we previously reported, the American Rescue Plan Act of 2021 (ARPA) was signed into law on March 11, 2021, requiring, among other things, the Pension Benefit Guaranty Corporation (PBGC) to issue its implementing regulations by July 9, 2021. As promised, PBGC issued an interim final rule, 86 Fed. Reg. 36598 (July 12, 2021) (the IFR), on a major element of the rescue plan―the Special Financial Assistance Program (SFA)―intended to provide a one-time payment to the estimated 200 most financially troubled multiemployer pension plans to help them survive and pay pensions through 2051. These 200 plans are a subset of the total of approximately 1,400 multiemployer pension plans covered by the ERISA insurance program. The IRS simultaneously issued Notice 2021-38 to provide guidance on how the SFA impacts minimum funding, as well as the reinstatement of certain suspended benefits by plans that receive the SFA.

This update describes key features of the IFR and IRS guidance, important not only to those multiemployer pension plans, and their participants and beneficiaries, but also to the employers who are obligated through their collective bargaining agreements (CBAs) to contribute to those plans. Even though the SFA calls upon eligible plans to apply for the payment, assuming they elect to receive it and comply with the detailed application process, contributing employers have good reason to monitor the activities of the plans that receive those employer contributions. Thus, beyond the key features of the SFA rules, this article also discusses what contributing employers may wish to monitor in those affected plans and what they may need to consider in terms of their own business planning.

I. Interim Final Rule

A. Who is Eligible for Financial Assistance?

ARPA, as explained by the IFR, provides that a multiemployer plan is eligible for financial assistance if it meets one or more of the following criteria:

- The plan is in critical and declining status for a plan year beginning in 2020, 2021, or 2022;

- the plan has been approved for “a suspension of benefits” on or before March 11, 2021 under the Multiemployer Pension Reform Act of 2014 (MPRA);

- the plan is certified by an actuary to be in critical status for a plan year beginning in 2020, 2021 or 2022, with a current liability funded percentage below 40% and with the plan having a ratio of active plan participants to inactive plan participants of less than 2 to 3; and/or

- “the plan became insolvent … after December 16, 2014, has remained insolvent, and has not been terminated . . . as of March 11, 2021.”

The IFR identifies certain plans that are not eligible, such as plans terminated by a mass withdrawal prior to January 1, 2020, plans terminated in a plan year that ended before January 1, 2020, or plans that elect to be in critical status, but do not otherwise meet the requirements for critical status.

For an eligible plan to receive SFA, the plan’s trustees must formally elect to receive the assistance, and in so doing, submit detailed information to PBGC for approval. The agency may require adjustments in the application, but the agency’s failure to act on the application within 120 days will result in the application being deemed approved.

The IFR also contains requirements aimed at ensuring uniformity in SFA applications. The IFR specifically instructs which data are to be used from a plan’s Form 5500 to determine whether a plan is in critical status for eligibility. To that end, the IFR contains direction on which actuarial assumptions are to be used in determining critical status or critical and declining status, drawing the line on the date the plan was zone certified. That is, if the certification of critical status or critical and declining status was issued prior to January 1, 2021, then PBGC will accept those assumptions that are incorporated into the certification, unless they are clearly erroneous. If a plan sponsor (that is, the plan’s board of trustees) applies for SFA and asserts eligibility based on a zone certification that was not accomplished prior to January 1, 2021, the plan sponsor must determine whether the plan is still in critical or critical and declining status using the same assumptions previously provided, unless those assumptions are now unreasonable.

Plans should consult their legal counsel to determine whether they meet eligibility requirements, and to ensure that appropriate information, assumptions, and other data points are used throughout the application process.

B. How Much SFA Can Eligible Plans Receive?

The IFR addresses a question left unanswered by the statute itself—how much financial assistance eligible plans may receive. Under ARPA, the amount of SFA available for eligible plans was to be “such amount required for the plan to pay all benefits due during the period beginning on the date of payment of the special financial assistance payment and ending on the last day of the plan year ending in 2051.” PBGC interpreted this to mean all of the plan’s existing and projected “obligations”—i.e, the sum of the present values of benefits and reinstated benefits, administrative expenses, etc.—in excess of “resources”—i.e, the present values of the fair market value of plan assets and the present value of future anticipated contributions, withdrawal liability payments, and other payments expected to be made to the plan—through the plan year ending in 2051. These projected amounts are calculated from the “measurement date,” which is the last day of the calendar quarter immediately preceding the date the plan’s application was filed, using certain interest rates, and consistent plan assumptions.

In drafting the IFR, PBGC has paid particular attention to ensure that electing plans do not inflate the amount of SFA which they may seek. The agency will scrutinize a plan’s revisions to any of its actuarial assumptions. In addition, the IFR specifically states that the amount of the SFA cannot be increased by virtue of certain events, including plan merger, asset transfers, benefit increases (other than required restorations of benefit suspension), and contribution decreases.

C. When Will the PBGC Process Applications and When Will Plans Receive Payment?

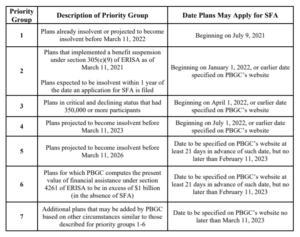

ARPA requires PBGC to process completed applications within 120 days of receipt; however, it allows the agency to establish a procedure to prioritize applications for the most financially troubled plans. The agency thus prioritized the application process into seven priority groups:

PBGC indicated that it will only accept as many applications as it can process in the required timeframe, after which it will temporarily close the electronic submission filing window and will not accept any additional applications. If the application is approved, the IFR provides that PBGC will typically provide relief in a one-time lump sum payment within 60 days after approval and no later than 90 days after approval.

If PBGC denies an application, the electing plan may accept the denial and revise the specific reason for the denial, without changing anything else in the application. The plan does not have to refile an entire application, but if it chooses to do so, it cannot change any of the underlying “base data” used in the denied application. PBGC notes that there is no limit to the number of times a plan may revise its application for SFA, except that the last revised application must be filed by the statutory deadline of December 31, 2026.

For plans that have been approved for a partition by PBGC before March 11, 2021, the agency provides an alternative process to file a single application with information about the original plan and the successor plan. Such application falls within the priority group 2, as identified above.

Plans should consult with their legal counsel and actuaries to ensure that the applications meet the requirements set forth by the IFR, and that they file before the appropriate deadlines.

D. What Restrictions Apply to SFA?

ARPA and the IFR place certain restrictions on how plans can use SFA funds. The SFA and earnings thereon—

- May only be used to make benefit payments and pay administrative expenses (Importantly, plans have broad discretion to use SFA funds to pay benefits and administrative expenses before using other plan assets);

- Must be segregated from other plan assets; and

- Must be invested in “investment grade” bonds or other permissible investments.

PBGC defines “investment grade” as “publicly traded securities for which the issuer has at least adequate capacity to meet the financial commitment under the security for the projected life of the asset or exposure.” The IFR identifies several types of investment grade bonds or investments, including exchange traded funds, mutual funds, and pooled trusts.

ARPA and the IFR also restrict plans receiving SFA from—

- Retroactively increasing benefits other than any required reinstatement of suspended benefits;

- Prospectively increasing benefits, unless an actuary certifies the reasonableness of the increase;

- Reducing contribution rates that were provided for in a CBA or plan document in effect on March 11, 2021;

- Transferring assets or liabilities, or engaging in a merger, or spinoff, without PBGC approval;

- Failing to invest plan assets in permissible investments; and

- Failing to meet certain annual reporting and audit requirements.

Notably, ARPA requires that plans receiving SFA reinstate any benefits that were suspended pursuant to the MPRA. The IRS, in conjunction with PBGC, issued Notice 2021-38, providing guidance on how these benefits are to be reinstated. Reinstated benefits must be paid in either a lump sum within three months of the date the SFA is received or in equal monthly installments over a five year period, beginning within three months of the date the SFA is received. These reinstated benefits are not subject to adjustments for interest. Retrospective and prospective benefit increases during the SFA coverage period, beyond benefits that are required to be reinstated, are barred unless special requirements are met. Plans must also adhere to specific administrative requirements, such as a notice to participants and beneficiaries and adoption of plan amendments.

To ensure compliance with these various nuances under ARPA and the IFR, plans should consult with legal counsel, prior to using the SFA they receive, to ensure the funds are allocated in a way that does not exceed the manner allowed under the law.

E. What Future Information and Guidance Will PBGC Provide?

In its IFR, PBGC repeatedly advises the public that updates relating to SFA will be provided on the agency’s website. Subjects to be covered on the website may include: the actuarial assumptions reflected in a plan’s application for SFA; the plan’s administrative expenses and contribution rates; the current status of filing windows; compliance with emergency filing requirements and substantiation of a claim of emergency status; withdrawal of an application for SFA; annual statements of compliance by plans receiving SFA; general instructions on SFA notice of benefit reinstatement; SFA instructions related to cash flow projections (Baseline); requirements for preparing the application for SFA; and information regarding the current priority group(s) for which applications are being accepted.

In contrast to subjects that will be addressed on its website, PBGC’s regulation states that “Unless confidential under the Privacy Act, all information that is filed with PBGC for an application for special financial assistance…may be made publicly available, at PBGC’s sole discretion, on PBGC’s website…or otherwise publicly disclosed.”

As suggested below, contributing employers may have a strong business interest in openness and transparency in PBGC’s management of the SFA program and the activities of any eligible plan(s) to which the employer contributes. It is unclear how PBGC will utilize the disclosure discretion it reserved. Once again, plans should work closely with counsel to stay apprised of developing legal and regulatory requirements that are being issued.

II. Employers’ Perspectives

Beyond the nuts and bolts of the IFR, and beyond the various nuances that the plans must navigate, employers that contribute to one or more of the 200 financially troubled plans will be interested in practical aspects on how to react to the unprecedented subsidy to certain plans.

SFA is an ambitious program providing its one-time payment intended to be sufficient to carry a troubled plan for 30 years, past future contingencies that cannot be clearly foreseen today. Moreover, SFA does not address the underlying problems plaguing troubled plans or the industries on which they depend.

But even apart from the dynamics of the modern business world, and as sophisticated as the interest and other assumptions applied to the plans may be, some experts have suggested that the SFA math does not add up. Interest and other rate projection issues are beyond the scope of this article, but employers that contribute to a troubled plan have a strong business interest in the prospects of the plan(s). The potential collapse of one or more plans, despite the SFA, may prompt employers to become more active in monitoring and analyzing the troubled plans to which they contribute.

Before suggesting an organized approach for an employer to monitor a plan dealing with SFA, it may be useful to focus on one subject of concern to many employers: withdrawal liability. The IFR suggests potential uncertainties that are difficult to predict. Besides the on-going structural problems dogging troubled plans—e.g., difficult demographics—the IFR requires that withdrawal liability be determined in different ways when compared to pre-ARPA rules. Plans may recognize SFA as a “resource,” and that would suggest a lower withdrawal liability. On the other hand, the interest rate used in the liability calculation will be drawn from the mass withdrawal rules, and that could have a hugely negative result for a withdrawing employer. Given that the purpose of the SFA subsidy is to aid troubled plans and their participants and beneficiaries, PBGC intends to prevent windfall situations for employers who might wish to withdraw from a plan.

The mass withdrawal interest rate rule noted above will continue for the later of ten years after receipt of SFA or the depletion of SFA funds. How long will that be? The IFR gives individual plans discretion to use SFA funds or other funds in paying its obligations. For this reason, it appears that a plan’s withdrawal liability calculation may have to use mass withdrawal interest assumptions for some period between ten and thirty years (i.e., ending in 2051). It remains to be seen how individual plans will exercise their discretion in prioritizing the use of SFA funds, and contributing employers may wish to monitor the plan’s asset management decisions more closely than in the past.

For withdrawal liability settlements over $50 million, PBGC must approve the settlement.

As if these uncertainties were not enough, Footnote 18 of the IFR states that “PBGC intends to propose a separate rule of general applicability…to prescribe actuarial assumptions which may be used by a plan actuary in determining an employer’s withdrawal liability.”

The factors described above suggest that PBGC may take a more active role in withdrawal liability matters in the future. Withdrawal liability is just one of the issues confronting contributing employers. Other issues may include the plan’s withdrawal rates when other employers withdraw, the overall demographics of the plan ten or twenty years from now, etc. Depending on how strongly a contributing employer believes its obligation to the plan affects the employer’s business interests, there are measures management may consider for the purpose of monitoring and analyzing the plan’s dealings with important issues in the next three decades.

Depending on the intensity of the views of the contributing employer’s management, the employer may consider one or more of the following measures going forward—

- Establish a management person or group to closely monitor the plan and PBGC. For example, someone might be tasked with reviewing the plan’s activities in applying for and utilizing SFA. That “someone” or group, might also be tasked with becoming familiar with the SFA activities of PBGC—for example, frequently checking the agency’s website postings, as suggested earlier in this article.

- Conduct research, analysis, and monitoring of PBGC’s administration of ARPA-related rules as they may impact the employer’s relationship with the plan and the employer’s overall business.

- Conduct research, analysis, and monitoring of the employer’s relationship with the plan and related options with a view to enhancing the company’s business position going forward. Included here might be calculations of the company’s withdrawal liability pre- and post-ARPA.

- Review and monitor the plan’s financial status, including its funding zone, and analyze the communications issued by the plan as to the issues facing it.

- Review the employer’s relations with its bargaining unit’s personnel and the union’s relationship with the plan. This might include clarification of the bargaining unit’s misunderstanding of the effect of SFA.

- Utilize legal counsel for matters that could involve issues with the employer’s continued relationship with the plan and the bargaining unit.

- Given the SFA’s heavy orientation to various actuarial rules affecting multiemployer plans, consider input from a management-side actuary who might provide technical analysis and other advice leading to options for negotiating with the bargaining unit or the plan as to future changes.

- Encourage the appropriate involvement of company personnel who have regular contact with the plan to ensure that any dealings with the plan are well coordinated.

In this unsettled time for financially troubled plans, contributing employers will be well served to be more rather than less focused on their employees’ multiemployer pension plans.